This tutorial explains the theoretical concepts of time series and ARIMA modeling and how we can forecast series using ARIMA with R.

Time Series

A time series is a data series consisting of several values over a time interval. e.g. daily Stock Exchange closing point, weekly sales and monthly profit of a company etc.

Typically, in a time series it is assumed that value at any given point of time is a result of its historical values. This assumption is the basis of performing a time series analysis. ARIMA technique exploits the auto-correlation (Correlation of observation with its lags) for forecasting.

So talking mathematically,

It means value (V) at time "t" is a function of value at time "n" instance ago with an error (e). Value at time "t" can depend on one or various lags of various order.

Example :

ARIMA (Box-Jenkins Approach)

ARIMA stands for Auto-Regressive Integrated Moving Average. It is also known as Box-Jenkins approach. It is one of the most popular techniques used for time series analysis and forecasting purpose.

ARIMA, as its full form indicates that it involves two components :

1. Auto-regressive Component

It implies relationship of a value of a series at a point of time with its own previous values. Such relationship can exist with any order of lag.

Lag -

Lag is basically value at a previous point of time. It can have various orders as shown in the table below. It hints toward a pointed relationship.

Many of the simple time series models are special cases of ARIMA Model

ARIMA Modeling with R : Steps and Code

Use ndiffs(),diff() functions to find the number of times differencing needed for the data & to difference the data respectively.

R Code : Treat Non- Stationary Data

The code below is just for demonstration. It does not hold for this example.

Fit a series of ARIMA models with combinations of p, d and q and select the model having minimum AIC / BIC.

R Code : Automatic Selection Algorithm

Final Model

#1. Residuals are Uncorrelated (White Noise)

#2. Residuals are normally distributed with mean zero

#3. Residuals have constant Variance

R Code :

For non-seasonal time series,

How auto.arima function works?

Steps and Code : ARIMA Modeling

Time Series

A time series is a data series consisting of several values over a time interval. e.g. daily Stock Exchange closing point, weekly sales and monthly profit of a company etc.

Typically, in a time series it is assumed that value at any given point of time is a result of its historical values. This assumption is the basis of performing a time series analysis. ARIMA technique exploits the auto-correlation (Correlation of observation with its lags) for forecasting.

So talking mathematically,

Vt = p(Vt-n) + e

It means value (V) at time "t" is a function of value at time "n" instance ago with an error (e). Value at time "t" can depend on one or various lags of various order.

Example :

Suppose Mr. X starts his job in year 2010 and his starting salary was $5,000 per month. Every years he is appraised and salary reached to a level of $20,000 per month in year 2014. His annual salary can be considered a time series and it is clear that every year's salary is function of previous year's salary (here function is appraisal rating).Tutorial - Basics of Time Series Modeling

ARIMA (Box-Jenkins Approach)

ARIMA stands for Auto-Regressive Integrated Moving Average. It is also known as Box-Jenkins approach. It is one of the most popular techniques used for time series analysis and forecasting purpose.

ARIMA, as its full form indicates that it involves two components :

- Auto-regressive component

- Moving average component

1. Auto-regressive Component

It implies relationship of a value of a series at a point of time with its own previous values. Such relationship can exist with any order of lag.

Lag -

Lag is basically value at a previous point of time. It can have various orders as shown in the table below. It hints toward a pointed relationship.

|

| Time Series : Lag |

2. Moving average components

It implies the current deviation from mean depends on previous deviations. Such relationship can exist with any number of lags which decides the order of moving average.

Moving Average -

Moving Average is average of consecutive values at various time periods. It can have various orders as shown in the table below. It hints toward a distributed relationship as moving itself is derivative of various lags.

It implies the current deviation from mean depends on previous deviations. Such relationship can exist with any number of lags which decides the order of moving average.

Moving Average -

Moving Average is average of consecutive values at various time periods. It can have various orders as shown in the table below. It hints toward a distributed relationship as moving itself is derivative of various lags.

|

| Moving Average Explanation |

Moving average is itself considered as one of the most rudimentary methods of forecasting. So if you drag the average formula in excel further (beyond Dec-15), it would give you forecast for next month.

Both Auto-regressive (lag based) and moving average components in conjunction are used by ARIMA technique for forecasting a time series.

ARIMA Modeling Steps

Both Auto-regressive (lag based) and moving average components in conjunction are used by ARIMA technique for forecasting a time series.

ARIMA Modeling Steps

- Plot the time series data

- Check volatility - Run Box-Cox transformation to stabilize the variance

- Check whether data contains seasonality. If yes, two options - either take seasonal differencing or fit seasonal arima model.

- If the data are non-stationary: take first differences of the data until the data are stationary

- Identify orders of p,d and q by examining the ACF/PACF

- Try your chosen models, and use the AICC/BIC to search for a better model.

- Check the residuals from your chosen model by plotting the ACF of the residuals, and doing a portmanteau test of the residuals. If they do not look like white noise, try a modified model.

- Check whether residuals are normally distributed with mean zero and constant variance

- Once step 7 and 8 are completed, calculate forecasts

Note : The auto.arima function() automates step 3 to 6.

Many of the simple time series models are special cases of ARIMA Model

- Simple Exponential Smoothing ARIMA(0,1,1)

- Holt's Exponential Smoothing ARIMA(0,2,2)

- White noise ARIMA(0,0,0)

- Random walk ARIMA(0,1,0) with no constant

- Random walk with drift ARIMA(0,1,0) with a constant

- Autoregression ARIMA(p,0,0)

- Moving average ARIMA(0,0,q)

ARIMA Modeling with R : Steps and Code

Data Set Description

Manufacturer’s stocks of evaporated and sweetened condensed milk (case goods), Jan 1971 – Dec 1980

Load Data

Step 2 : How to detect Seasonality

Seasonality usually causes the series to be nonstationary because the average values at some particular times within the seasonal span (months, for example) may be different than the average values at other times.

R Code : Detect Seasonality

1. Seasonal differencing

It is defined as a difference between a value and a value with lag that is a multiple of S. With S = 4, which may occur with quarterly data, a seasonal difference is

(1-B4)xt = xt - xt-4.

2. Differencing for Trend and Seasonality:

When both trend and seasonality are present, we may need to apply both a non-seasonal first difference and a seasonal difference.

3. Fit Seasonal ARIMA Model

The stationarity of the data can be known by applying Unit Root Tests - Augmented Dickey–Fuller test (ADF), Kwiatkowski-Phillips-Schmidt-Shin (KPSS) test.

R Code : Detect Non-Stationary Data

Since p-value of KPSS (0.1) is greater than 0.05, it indicates series is stationary. The p-value of ADF also indicates stationary series.

In this example, the series is already stationary so we don't need to make any treatment. If the data is non- stationary, then we use Differencing - computing the differences between consecutive observations.

First difference of a time series

library(forecast)

library(fpp)

# Plot time series data

tsdisplay(condmilk)

|

| Time Series Plot |

Step I : Check Volatility

If the data show different variation at different levels of the series, then a transformation can be beneficial. Apply box cox transformation to find the best transformation technique to stabilize the variance.

Lambda values :

λ = 1 (No substantive transformation)

λ = 0.5 (Square root plus linear transformation)

λ = 0 (Natural logarithm)

λ = −1 (Inverse plus 1)

Note : InvBoxCox() function reverses the transformation.R Code : Check Volatility

lambda = BoxCox.lambda(condmilk)

tsdata2 = BoxCox(condmilk, lambda=lambda)

tsdisplay(tsdata2)

Step 2 : How to detect Seasonality

R Code : Detect Seasonality

seasonplot(condmilk)How to treat Seasonality

monthplot(condmilk)

1. Seasonal differencing

It is defined as a difference between a value and a value with lag that is a multiple of S. With S = 4, which may occur with quarterly data, a seasonal difference is

(1-B4)xt = xt - xt-4.

2. Differencing for Trend and Seasonality:

When both trend and seasonality are present, we may need to apply both a non-seasonal first difference and a seasonal difference.

3. Fit Seasonal ARIMA Model

The seasonal ARIMA model incorporates both non-seasonal and seasonal factors in a multiplicative model. One shorthand notation for the model is

ARIMA(p, d, q) × (P, D, Q)S

with p = non-seasonal AR order, d = non-seasonal differencing, q = non-seasonal MA order, P = seasonal AR order, D = seasonal differencing, Q = seasonal MA order, and S = time span of repeating seasonal pattern.

Step 3 : Detect Non-Stationary DataThe stationarity of the data can be known by applying Unit Root Tests - Augmented Dickey–Fuller test (ADF), Kwiatkowski-Phillips-Schmidt-Shin (KPSS) test.

Augmented Dickey–Fuller test (ADF)

The null-hypothesis for an ADF test is that the data are non-stationary. So p-value greater than 0.05 indicates non-stationarity, and p-values less than 0.05 suggest stationarity.KPSS Test

In this case, the null-hypothesis is that the data are stationary. In this case, p-value less than 0.05 indicates non-stationary series and p-value greater than 0.05 indicates stationary series.

R Code : Detect Non-Stationary Data

# Unit Ratio Tests

library(tseries)

adf = adf.test(tsdata2)

kpss = kpss.test(tsdata2)

adf

kpss

Since p-value of KPSS (0.1) is greater than 0.05, it indicates series is stationary. The p-value of ADF also indicates stationary series.

How to treat Non-Stationary Data

First difference of a time series

It is the difference of the current value from the lagged value. The first difference of Y at period t is equal to Yt-Yt-1. The calculation is shown below in the image.

|

| First Differencing Calculation |

Use ndiffs(),diff() functions to find the number of times differencing needed for the data & to difference the data respectively.

R Code : Treat Non- Stationary Data

# Number of Difference Required to make data stationaryIn this example, series is stationary. Hence, we don't need to perform treatment to make it stationary.

ndiffs(tsdata2)

The code below is just for demonstration. It does not hold for this example.

tsdata3 = diff(tsdata2, differences = 1)

plot.ts(tsdata3)

Step 4 : Model Identification and Estimation

We can do the model identification in two ways :

1 . Using ACF and PACF Functions

2. Using Minimum Information Criteria Matrix (Recommended)

Method I : ACF and PACF Functions

Autocorrelation Function (ACF)

Autocorrelation is a correlation coefficient. However, instead of correlation between two different variables, the correlation is between two values of the same variable at times Xt and Xt-h. Correlation between two or more lags.

If the autocorrelation at lag 1 exceeds the significance bounds, set q = 1

If the time series is a moving average of order 1, called a MA(1), we should see only one significant autocorrelation coefficient at lag 1. This is because a MA(1) process has a memory of only one period. If the time series is a MA(2), we should see only two significant autocorrelation coefficients, at lag 1 and 2, because a MA(2) process has a memory of only two periods.

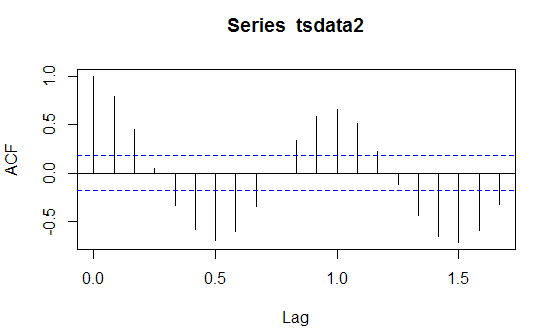

R Code : ACF

R Code : ACF

acf(tsdata2, lag.max = 20)

|

| ACF |

Partial Autocorrelation Function (PACF)

For a time series, the partial autocorrelation between xt and xt-h is defined as the conditional correlation between xt and xt-h, conditional on xt-h+1, ... , xt-1, the set of observations that come between the time points t and t−h.

If the partial autocorrelation at lag 1 exceeds the significance bounds, set p = 1

If the time-series has an autoregressive order of 1, called AR(1), then we should see only the first partial autocorrelation coefficient as significant. If it has an AR(2), then we should see only the first and second partial autocorrelation coefficients as significant.

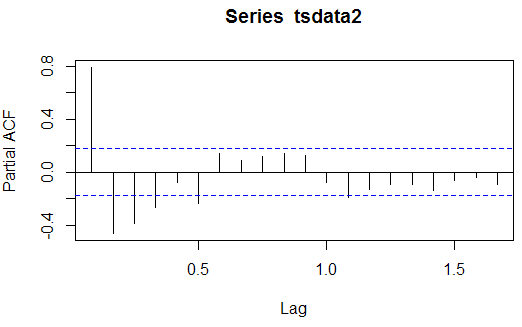

R Code : PACF

R Code : PACF

pacf(tsdata2, lag.max = 20)

|

| PACF |

Method II : Minimum AIC / BIC Criteria

R Code : Automatic Selection Algorithm

#Automatic Selection Algorithm - Fast

auto.arima(tsdata2, trace= TRUE, ic ="aicc", approximation = FALSE)

#Auto Algorithm - Slow but more accurate

auto.arima(tsdata2, trace= TRUE, ic ="aicc", approximation = FALSE, stepwise = FALSE)

Final Model

finalmodel = arima(tsdata2, order = c(0, 0, 3), seasonal = list(order = c(2,0,0), period = 12))Compare Multiple Models

summary(finalmodel)

AIC(arima(tsdata2, order = c(1, 0, 0), seasonal = list(order = c(2,0,0), period = 12)),Residual Diagnostics

arima(tsdata2, order = c(2, 0, 0), seasonal = list(order = c(2,0,0), period = 12)),

arima(tsdata2, order = c(0, 0, 3), seasonal = list(order = c(2,0,0), period = 12)))

#1. Residuals are Uncorrelated (White Noise)

#2. Residuals are normally distributed with mean zero

#3. Residuals have constant Variance

R Code :

# Check whether the residuals look like white noise (Independent)

# p>0.05 then the residuals are independent (white noise)

tsdisplay(residuals(finalmodel))

Box.test(finalmodel$residuals, lag = 20, type = "Ljung-Box")

# p-values shown for the Ljung-Box statistic plot are incorrect so calculate

#critical chi squared value

# Chi-squared 20 d.f. and critical value at the 0.05

qchisq(0.05, 20, lower.tail = F)

# Observed Chi-squared 13.584 < 31.41 so we don't reject null hypothesis

# It means residuals are independent or uncorrelated (white noise) at lags 1-20.

# whether the forecast errors are normally distributedHow to choose the number of lags for the Ljung-Box test

qqnorm(finalmodel$residuals); qqline(finalmodel$residuals) # Normality Plot

For non-seasonal time series,

Number of lags to test = minimum (10, length of time series / 5)For seasonal time series,

or simply take 10

Number of lags to test = minimum (2m, length of time series / 5)Forecasting

where, m = period of seasonality

or simply take 2m

# predict the next 5 periodsNote : If lambda specified, forecasts back-transformed via an inverse Box-Cox transformation.

Forecastmodel = forecast.Arima(finalmodel, h = 5, lambda = lambda)

If you have a fitted arima model, you can use it to forecast other time series.

inpt = arima(newdata, model=Forecastmodel)Appendix

How auto.arima function works?

auto.arima(kingsts, approximation=FALSE, start.p=1, start.q=1, trace=TRUE, seasonal=TRUE)

1. The number of differences d is determined using repeated KPSS tests.

2. The values of p and q are then chosen by minimizing the AIC after differencing the data d times. Rather than considering every possible combination of p and q, the algorithm uses a stepwise search to traverse the model space.

(a) The best model (with smallest AICc) is selected from the following four:

ARIMA(2,d,2),

ARIMA(0,d,0),

ARIMA(1,d,0),

ARIMA(0,d,1).

If d=0 then the constant c is included; if d≥1 then the constant c is set to zero. This is called the "current model".

(b) Variations on the current model are considered:

vary p and/or q from the current model by ±1;

include/exclude c from the current model.

The best model considered so far (either the current model, or one of these variations) becomes the new current model.

(c) Repeat Step 2(b) until no lower AICc can be found.

Steps and Code : ARIMA Modeling

Deepanshu founded ListenData with a simple objective - Make analytics easy to understand and follow. He has over 10 years of experience in data science. During his tenure, he worked with global clients in various domains like Banking, Insurance, Private Equity, Telecom and HR.

Very well written !

ReplyDeleteHi Need password to open the excel file . pls provide

ReplyDeletehi please tell me the password for excell please i have do to some project work but i dont know how work ARIMA model, please tell me the password or send me the password to my mail id peddollakishore@gmail.com

ReplyDeleteThe code is already available for use in the article. The excel sheet is for my personal use.

DeleteGood job listendata! I'll keep your site on my bookmarks.

ReplyDeleteHi Deepanshu,

ReplyDeleteCan you provide any data set where I can practice the same ARIMA modeling codes or the same data set which you have used at khushboogirotra@gmail.com

you may find financial time series data for stocks from yahoo finance useful for this purpose.

Deletenice work done. Please i need more explanation on how to choose the AR and MA using ACF and PACF plots

ReplyDeleteShould it not be tadata3 instead of tsdata2 as you are supposed to run ARIMA model on the differenced data?

ReplyDeletefinalmodel = arima(tsdata2, order = c(0, 0, 3), seasonal = list(order = c(2,0,0), period = 12))

Please let me know if the model needs to run on Box-Cox transformed data (tsdata2) of differenced data (tsdata3)?

Hi Deepanshu. In the following lines of code, how did you get the OBSERVED value of Chi-squared?

ReplyDelete# Chi-squared 20 d.f. and critical value at the 0.05

qchisq(0.05, 20, lower.tail = F)

# Observed Chi-squared 13.584 < 31.41 so we don't reject null hypothesis

How use xts() and ts() function inside for loop?

ReplyDeleteplease send a ARIMA model excel sheet dataset to my mail id-gomsrenu296@gmail.com

ReplyDelete