This tutorial explains the steps to build a logistic regression model in Excel using a practical example. It also covers how to calculate the following metrics of logistic regression in Excel.

- Coefficient Table : Coefficients, P-Value, Standardized Coefficients, Odds Ratio etc.

- Model Performance Metrics : AUC, AIC, Confusion Matrix etc.

- Scoring or predicting outcomes for new data

Logistic regression is a statistical technique used for binary classification tasks. It is used when dependent variable has two possible values such as 0 and 1. For example : success/failure, attrition/retention etc.

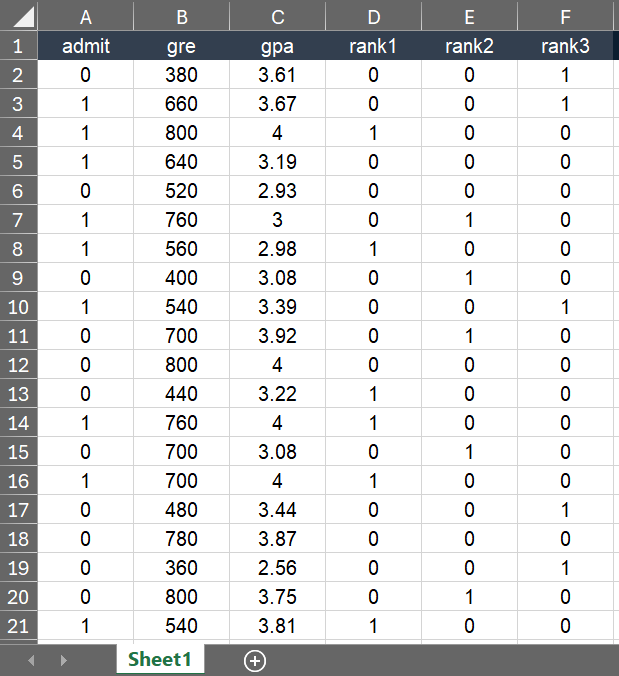

Suppose you are asked to perform logistic regression analysis in Excel to check whether a student will be admitted or not into graduate school based on their GRE and GPA grades along with the ranking of the undergraduate school they attended.

The raw data looks like the image shown below. We have 397 observations and 5 independent variables in our dataset. Data are in range A2:F398 in Excel. The column admit is a binary dependent variable in this case and the remaining columns contain data for independent variables.

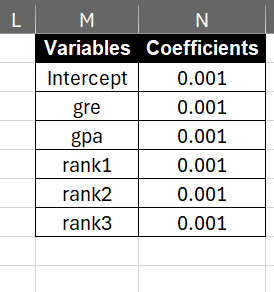

Step 1 : Setting Initial Coefficients

In this step, we are creating a coefficient table for independent variables and intercept. We are setting each coefficient to 0.001. Later we will be adjusting them to maximize the log likelihood.

- Enter intercept and independent variable names in range M2:M7.

- Enter initial values for coefficients as 0.001 in range N2:N7.

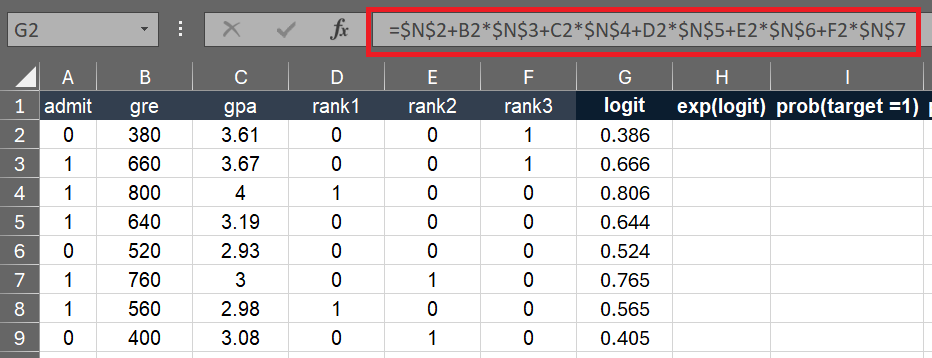

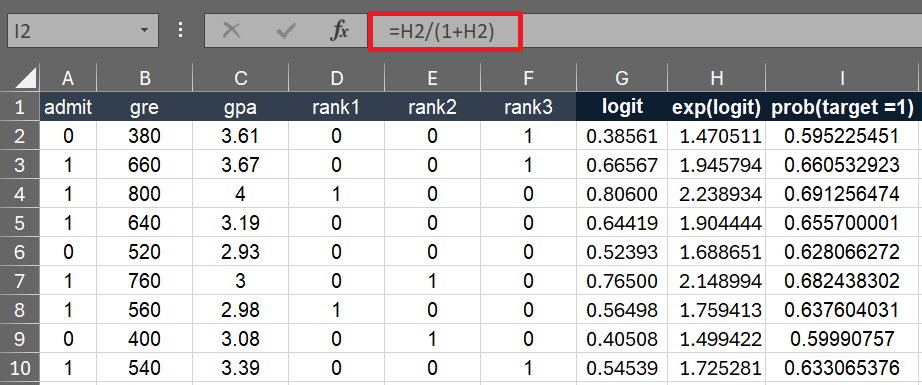

Step 2 : Calculations of Logistic Regression

It is linear combination of the independent variables weighted by their coefficients. To calculate logit, we need to multiply coefficients with values of independent variables and then sum them.

In Excel, enter the following formula in cell G2 and then paste it down to the last row i.e cell G398.

=$N$2+B2*$N$3+C2*$N$4+D2*$N$5+E2*$N$6+F2*$N$7

Alternative Method : If you have a lot of independent variables, it is inefficient to write out the lengthy formula above. Alternatively, you can use the SUMPRODUCT formula.

=$N$2+SUMPRODUCT(B2:F2,TRANSPOSE($N$3:$N$7))

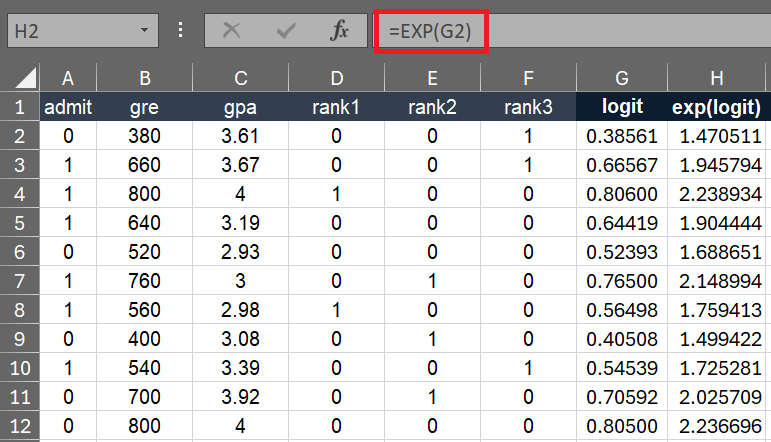

In this step, we simply take exponential value of the logit using the Excel's EXP() function. In cell H2, enter the following formula.

=EXP(G2)

The probability that the dependent variable y is 1 is calculated as:

prob(y=1) = exp(logit) / (1 + exp(logit))

In cell I2, enter the following formula and then paste it down to cell I398.

=H2/(1+H2)

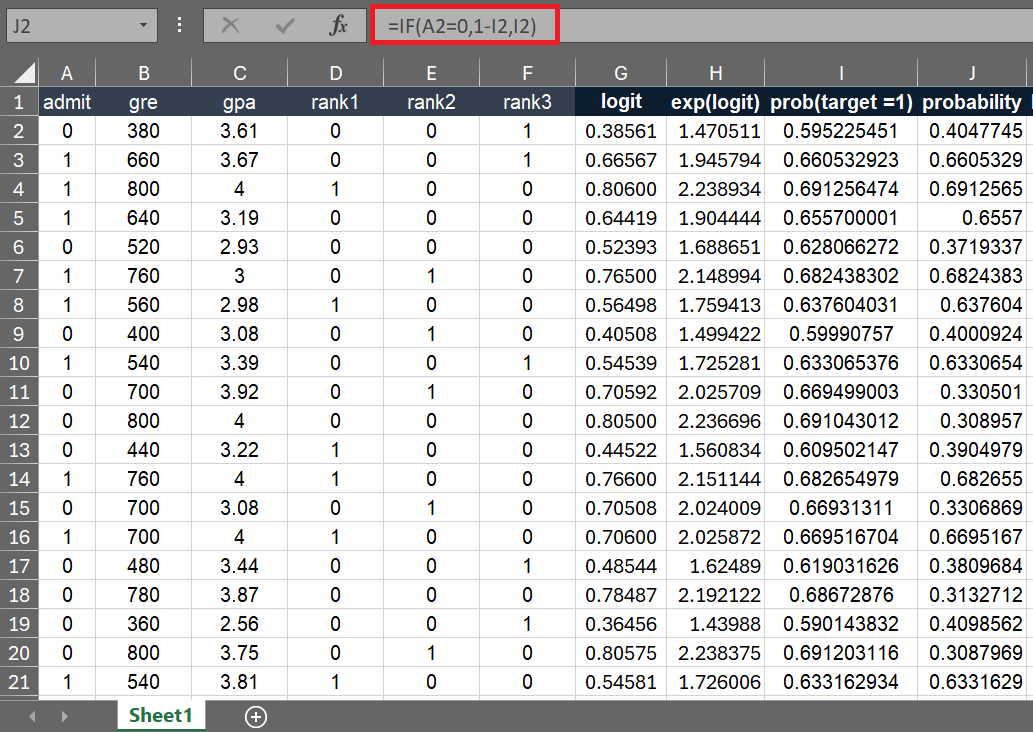

In this step, we are calculating the probability of the dependent variable (y) is either 0 or 1.

prob(y=0) = 1 - prob(y=1)

In cell J2, enter the following formula and then paste it down to cell J398.

=IF(A2=0,1-I2,I2)

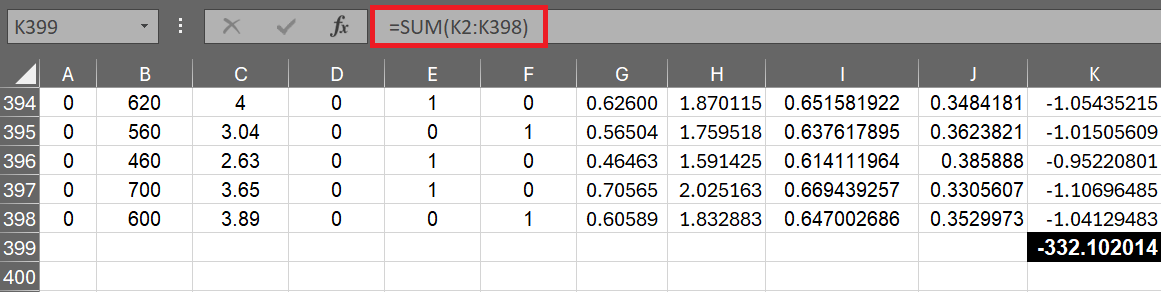

To calculate the log likelihood, we need to take the natural log of predicted probabilities.

In cell K2, enter the following formula to calculate the log likelihood and then paste it down to cell K398.

=LN(J2)

Next step is to sum the log likelihood for each observation. In the last row of the column i.e. cell K399, sum this column.

=SUM(K2:K398)

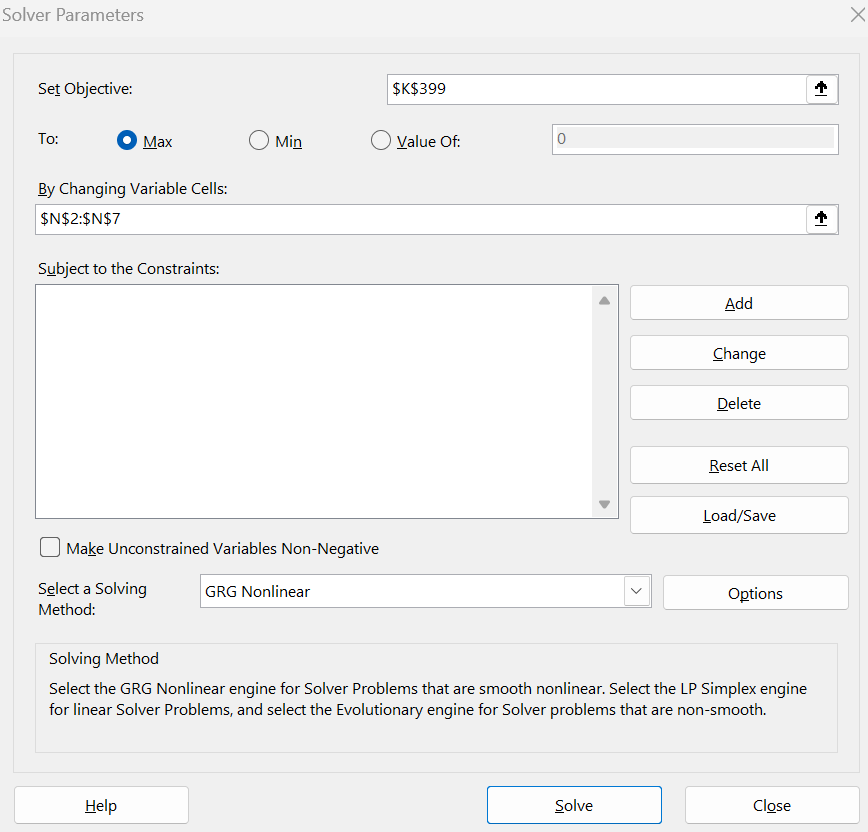

Step 3 : Maximizing Log Likelihood

In this step, we need to adjust the coefficients to maximize the log likelihood.

Excel's solver add-in will be used to optimizate the likelihood function.

After installing the solver add-in, follow the steps below.

- Go to the "Data" tab and click on "Solver".

- Set the objective function to the cell K399 containing the sum of the log-likelihood.

- Select "Max" in the "To:" section.

- By Changing Variable Cells: Select cells N2:N7 containing coefficients (including intercept).

- Make Unconstrained Variables Non-Negative: Uncheck this option.

- Choose the Solver engine GRG Nonlinear.

- Click "Solve" to run the optimization.

The final logistic regression coefficients and predicted probabilities are shown below.

Suppose you have a new data which was not used to build the logistic regression model. You need to estimate the predicted probability for the new data using the model you built in the previous steps.

| gre | gpa | rank1 | rank2 | rank3 |

|---|---|---|---|---|

| 650 | 3.67 | 0 | 0 | 1 |

All you need to do is drag the formula down (as shown in the previous steps) to the new data to calculate prob(y=1). Refer to the image below.

The standard error of a coefficient in logistic regression explains how reliable coefficient estimates are.

To calculate the standard error of coefficients, run the VBA code below.

Sub StandardErrors()

Dim XData As String

Dim MatrixSize As Long

Dim CoeffData As String

Dim outputStartingCell As String

Dim i As Long, j As Long

Dim Hessian() As Double

Dim ws As Worksheet

' Set input values

Set ws = ThisWorkbook.Sheets("Sheet1") ' Change sheet name if needed

XData = "B2:F398" ' Range for independent variables

CoeffData = "N2:N7" ' Range for coefficients (incld. intercept)

outputStartingCell = "O2" ' Starting cell where you want to populate standard errors (output)

' Initialize the Hessian matrix

MatrixSize = Range(XData).Columns.Count + 1 ' Include intercept

ReDim Hessian(1 To MatrixSize, 1 To MatrixSize)

' Read coefficient values from cells (adjust cell references as needed)

Dim Coeff() As Double

Dim rng As Range

Set rng = ws.Range(CoeffData) ' Convert the string to a range

ReDim Coeff(1 To rng.Cells.Count)

i = 1

For Each cell In rng

Coeff(i) = cell.Value

i = i + 1

Next cell

' Read feature data from cells (adjust cell references as needed)

Dim X() As Double

Dim inputRange As Range

Set inputRange = ws.Range(XData)

n = inputRange.Rows.Count

ReDim X(1 To n, 1 To MatrixSize)

Dim rowIndex As Long, colIndex As Long

For rowIndex = 1 To n

X(rowIndex, 1) = 1 ' Intercept

For colIndex = 1 To MatrixSize - 1

X(rowIndex, colIndex + 1) = inputRange.Cells(rowIndex, colIndex).Value

Next colIndex

Next rowIndex

' Calculate the Hessian matrix

Dim p_hat() As Double

ReDim p_hat(1 To n)

For rowIndex = 1 To n

Dim Xb As Double

Xb = 0

For j = 1 To MatrixSize

Xb = Xb + X(rowIndex, j) * Coeff(j)

Next j

p_hat(rowIndex) = Exp(Xb) / (1 + Exp(Xb)) ' Predicted probabilities

Next rowIndex

' Calculate the Hessian elements

For i = 1 To MatrixSize

For j = 1 To MatrixSize

Dim sum_term As Double

sum_term = 0

For rowIndex = 1 To n

sum_term = sum_term + X(rowIndex, i) * X(rowIndex, j) * p_hat(rowIndex) * (1 - p_hat(rowIndex))

Next rowIndex

Hessian(i, j) = sum_term

Next j

Next i

' Invert the Hessian matrix

Dim invHessian() As Double

invHessian = InverseMatrix(Hessian)

' Calculate standard errors

Dim se() As Double

ReDim se(1 To MatrixSize)

For i = 1 To MatrixSize

se(i) = Sqr(invHessian(i, i))

Next i

' Output standard errors to the worksheet

ws.Range(outputStartingCell).Value = se(1) ' Intercept

For i = 2 To MatrixSize

ws.Range(outputStartingCell).Offset(i - 1, 0).Value = se(i)

Next i

End Sub

Function InverseMatrix(mat() As Double) As Variant

' This function computes the inverse of a matrix using the Gaussian elimination method

' Note: This function assumes that the input matrix is square and invertible

Dim n As Long

n = UBound(mat, 1)

Dim augmented() As Double

ReDim augmented(1 To n, 1 To 2 * n)

Dim i As Long, j As Long, k As Long

Dim factor As Double

' Create augmented matrix [mat | I]

For i = 1 To n

For j = 1 To n

augmented(i, j) = mat(i, j)

augmented(i, j + n) = IIf(i = j, 1, 0)

Next j

Next i

' Perform Gaussian elimination

For i = 1 To n

' Make the diagonal element 1

factor = augmented(i, i)

For j = 1 To 2 * n

augmented(i, j) = augmented(i, j) / factor

Next j

' Make the other elements in the column 0

For k = 1 To n

If k <> i Then

factor = augmented(k, i)

For j = 1 To 2 * n

augmented(k, j) = augmented(k, j) - factor * augmented(i, j)

Next j

End If

Next k

Next i

' Extract the inverse matrix

Dim invMat() As Double

ReDim invMat(1 To n, 1 To n)

For i = 1 To n

For j = 1 To n

invMat(i, j) = augmented(i, j + n)

Next j

Next i

InverseMatrix = invMat

End Function

- In Excel, open the VBA editor by pressing Alt + F11 keyboard shortcut key.

- Select Insert > Module to create a module.

- Paste the above macro code in the module.

- Close the VBA editor by clicking the 'X' in the top-right corner.

- Run the macro by pressing Alt + F8 and select "StandardErrors" macro

Set ws = ThisWorkbook.Sheets("Sheet1"): Change "Sheet1" to your desired sheet name.XData = "B2:F398": Specifies the range for independent variables. Modify "B2:F398" to match your data range.CoeffData = "N2:N7": Defines the range for coefficients including the intercept. Adjust "N2:N7" to the range for your coefficients.outputStartingCell = "O2": Sets the starting cell for outputting results. Change "O2" to the cell where you want to begin outputting data.

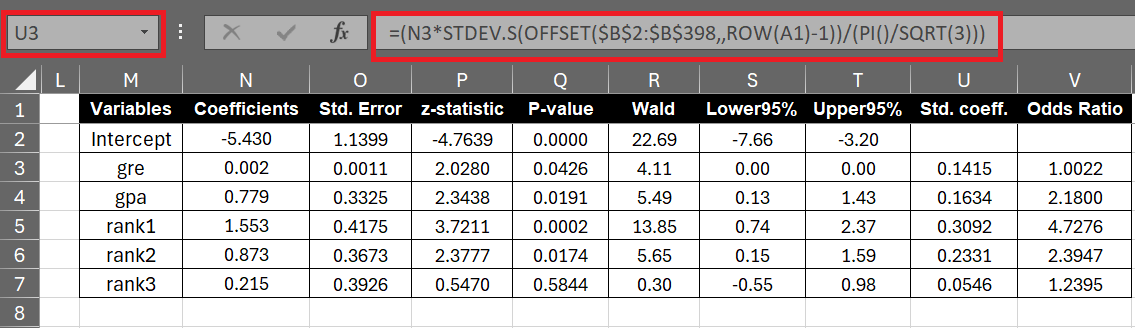

The z-statistic measures how many standard deviations a coefficient estimate is away from 0. A small p-value less than 0.05 means the coefficient of independent variable is significantly different from 0.

z-statistic = coefficient / standard error

To calculate z-statistic, enter the following formula in cell P2. Cell N2 contains coefficients and cell O2 contains standard error.

=N2 / O2

To calculate p-value, enter the following formula in cell Q2.

=2*(1-NORM.S.DIST(ABS(N2)/O2,1))

To calculate wald chi-square, all we need to do is to take square of z-statistics. In cell R2, enter the following formula.

=P2^2

The formula for calculating confidence intervals for a coefficient is as follows:

CI = coefficient ± z * Standard Error

Here z is the critical value. It is 1.96 for a 95% confidence interval

In cell S2, enter the following formula for lower confidence interval.

=N2 - 1.96*O2

In cell T2, enter the following formula for upper confidence interval.

=N2 + 1.96*O2

Standardized Coefficients help in understanding the relative importance of each independent variable. Variable with the largest absolute value of a standardized coefficient means the most important variable.

The formula for calculating confidence intervals for a coefficient is as follows:

Standardized Coefficient = (β * SDX) / (π / √3)

SDX is a standard deviation of an independent variable.

In cell U3, enter the following formula. Please note that it is not entered against intercept. Paste the formula down to the cells below to get standardized coefficients for each independent variable. In this formula, cell N3 refers to unstandardized coefficient; range B2:B398 refers to raw values of variable. By using the OFFSET function, this formula became dynamic and automatically changing the range of variables as it's pasted down.

=(N3*STDEV.S(OFFSET($B$2:$B$398,,ROW(A1)-1))/(PI()/SQRT(3)))

Odds ratio is exponential value of a coefficient. It means how the odds of the dependent variable change with each unit change in the independent variable.

In cell V3, enter the following formula to calculate odds ratio in Excel.

=EXP(N3)

The main model performance metrics of logistic regression are Area Under Curve (AUC) of the ROC Curve, AIC and Hosmer-Lemeshow (HL) Test.

AUC measures how well the model can differentiate between events (1) and non-events (0).

Insert the following VBA code by following the first four steps shown in this section of article.

Function AUROC(predictions As Range, actuals As Range) As Double

Dim n As Long

Dim tpr() As Double, fpr() As Double

Dim sorted_indices() As Long

Dim i As Long

' Check if the predictions and actuals ranges have the same number of elements

If predictions.Count <> actuals.Count Then

MsgBox "Predictions and actuals must have the same number of elements."

AUROC = -1

Exit Function

End If

n = predictions.Count

ReDim tpr(0 To n + 1), fpr(0 To n + 1)

' Sort predictions and actuals in descending order of predictions

sorted_indices = SortIndicesDescending(predictions)

Dim num_pos As Long, num_neg As Long

num_pos = WorksheetFunction.CountIf(actuals, 1)

num_neg = n - num_pos

If num_pos = 0 Or num_neg = 0 Then

MsgBox "There must be both positive and negative actual values."

AUROC = -1

Exit Function

End If

Dim tp_count As Long, fp_count As Long

tp_count = 0

fp_count = 0

' Calculate TPR and FPR for each threshold

For i = 1 To n

If actuals.Cells(sorted_indices(i)).Value = 1 Then

tp_count = tp_count + 1

Else

fp_count = fp_count + 1

End If

tpr(i) = tp_count / num_pos

fpr(i) = fp_count / num_neg

Next i

' Append (0,0) and (1,1) to the ROC curve

tpr(0) = 0

tpr(n + 1) = 1

fpr(0) = 0

fpr(n + 1) = 1

' Calculate AUC from the ROC curve using trapezoidal rule

Dim auc As Double

auc = 0

For i = 1 To n

auc = auc + (tpr(i) + tpr(i - 1)) * (fpr(i - 1) - fpr(i)) / 2

Next i

' Ensure AUC is non-negative

AUROC = Abs(auc)

End Function

Function SortIndicesDescending(predictions As Range) As Variant

Dim i As Long, j As Long

Dim temp As Double

Dim indices() As Long

Dim sorted_predictions() As Double

Dim n As Long

n = predictions.Count

ReDim indices(1 To n)

ReDim sorted_predictions(1 To n)

For i = 1 To n

indices(i) = i

sorted_predictions(i) = predictions.Cells(i).Value

Next i

' Simple bubble sort

For i = 1 To n - 1

For j = i + 1 To n

If sorted_predictions(i) < sorted_predictions(j) Then

' Swap predictions

temp = sorted_predictions(i)

sorted_predictions(i) = sorted_predictions(j)

sorted_predictions(j) = temp

' Swap indices

temp = indices(i)

indices(i) = indices(j)

indices(j) = temp

End If

Next j

Next i

SortIndicesDescending = indices

End Function

After inserting the above code into the module, you can use the function =AUROC(prob(y=1),dependent variable) in any cell within your Excel workbook.

=AUROC(I2:I398,A2:A398)

AUC is used for model selection. Lower AIC values means better-fitting models. It penalizes models for their complexity and favors simpler models that explain the data well.

AIC = −2×log-likelihood+2×(Number of Independent Variables+1)

Cells K2:K398 refers to range of log-likelihood column. Cells B1:F1 refers to headers of independent variables.

=-2*SUM(K2:K398)+2*(COUNTA(B1:F1)+1)

A confusion matrix is used to evaluate the performance of a classification model. It compares the actual values with the model's predictions. You can refer to this tutorial - Confusion Matrix in Excel

The Hosmer-Lemeshow (HL) test is used to check the goodness of fit of a logistic regression model. It explains how well the predicted probabilities from the model match the actual outcomes.

Calculating Hosmer-Lemeshow (HL) Test in Excel

Deepanshu founded ListenData with a simple objective - Make analytics easy to understand and follow. He has over 10 years of experience in data science. During his tenure, he worked with global clients in various domains like Banking, Insurance, Private Equity, Telecom and HR.

Share Share Tweet